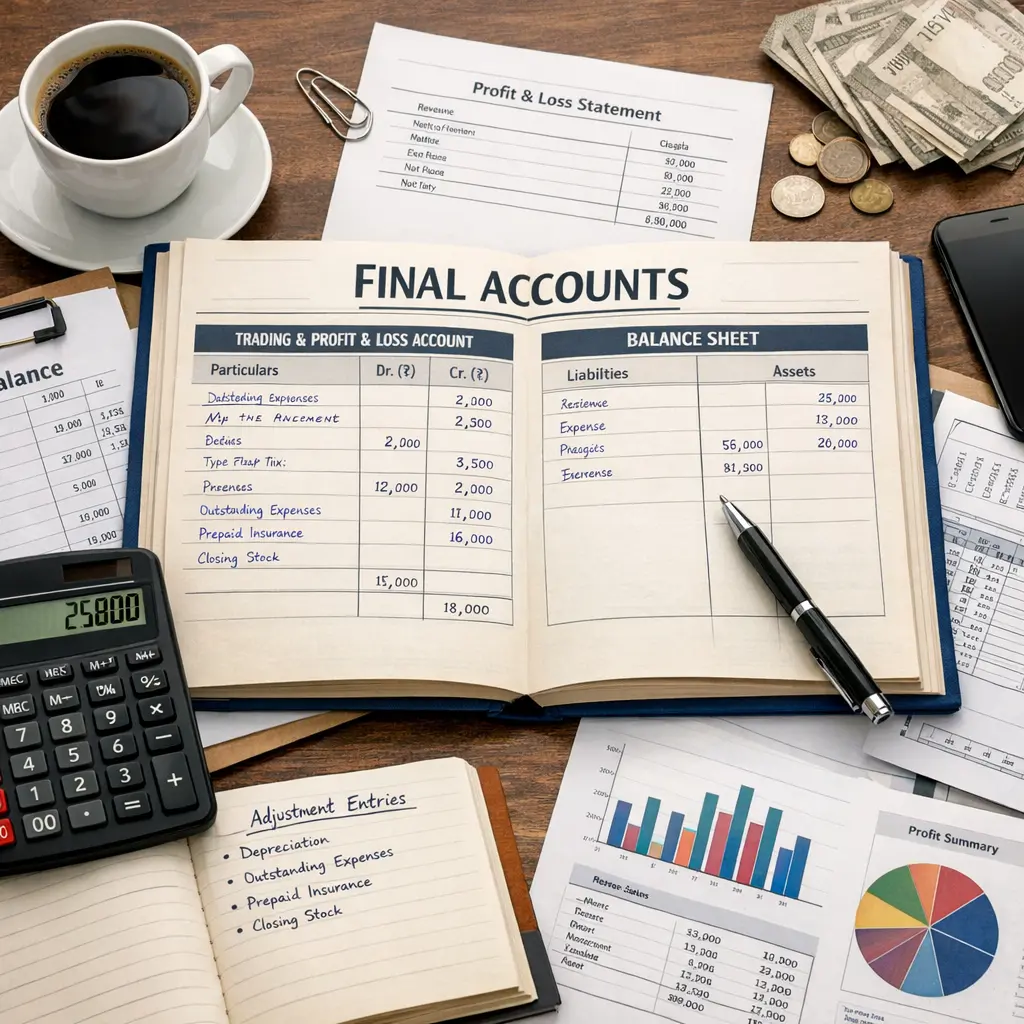

Final Account Preparation+50

Final Account Preparation in Financial Management and Business Practices refers to the process of compiling and presenting a company’s financial statements at the end of an accounting period. This includes the preparation of the trading account, profit and loss account, and balance sheet. The process ensures that all financial transactions are accurately recorded, summarized, and reported, providing stakeholders with a clear view of the organization’s financial position and performance for informed decision-making.

Final Account Preparation+50

Final Account Preparation in Financial Management and Business Practices refers to the process of compiling and presenting a company’s financial statements at the end of an accounting period. This includes the preparation of the trading account, profit and loss account, and balance sheet. The process ensures that all financial transactions are accurately recorded, summarized, and reported, providing stakeholders with a clear view of the organization’s financial position and performance for informed decision-making.

💡 Key Takeaways

- Explain the purpose and main components of final accounts (Trading, Profit and Loss, and Balance Sheet).

- Apply common year-end adjustments (depreciation, accruals and prepayments, bad debts and provisions) to prepare accurate figures.

- Prepare a Trading and Profit and Loss account and a Balance Sheet from a trial balance with those adjustments.

- Read and interpret the final accounts to judge profitability, liquidity, and financial position.

❓ Frequently Asked Questions

What is the purpose of final accounts?

Final accounts summarize a period's financial performance and position, typically including trading results, net profit or loss, and the financial position at period end.

What are the main components of final accounts?

Trading account (gross profit/loss), Profit & Loss account (net profit or loss after expenses), and Balance Sheet (assets, liabilities, and owner's equity).

Which adjustments are commonly made before finalizing accounts?

Accruals and prepayments, depreciation, provisions for bad debts, stock adjustments (closing stock), and incomes/expenses received or paid in advance.

How are closing stock and depreciation treated in final accounts?

Closing stock affects cost of goods sold in the trading account; depreciation reduces asset value and is recorded as an expense in the P&L and lowers the asset on the Balance Sheet.