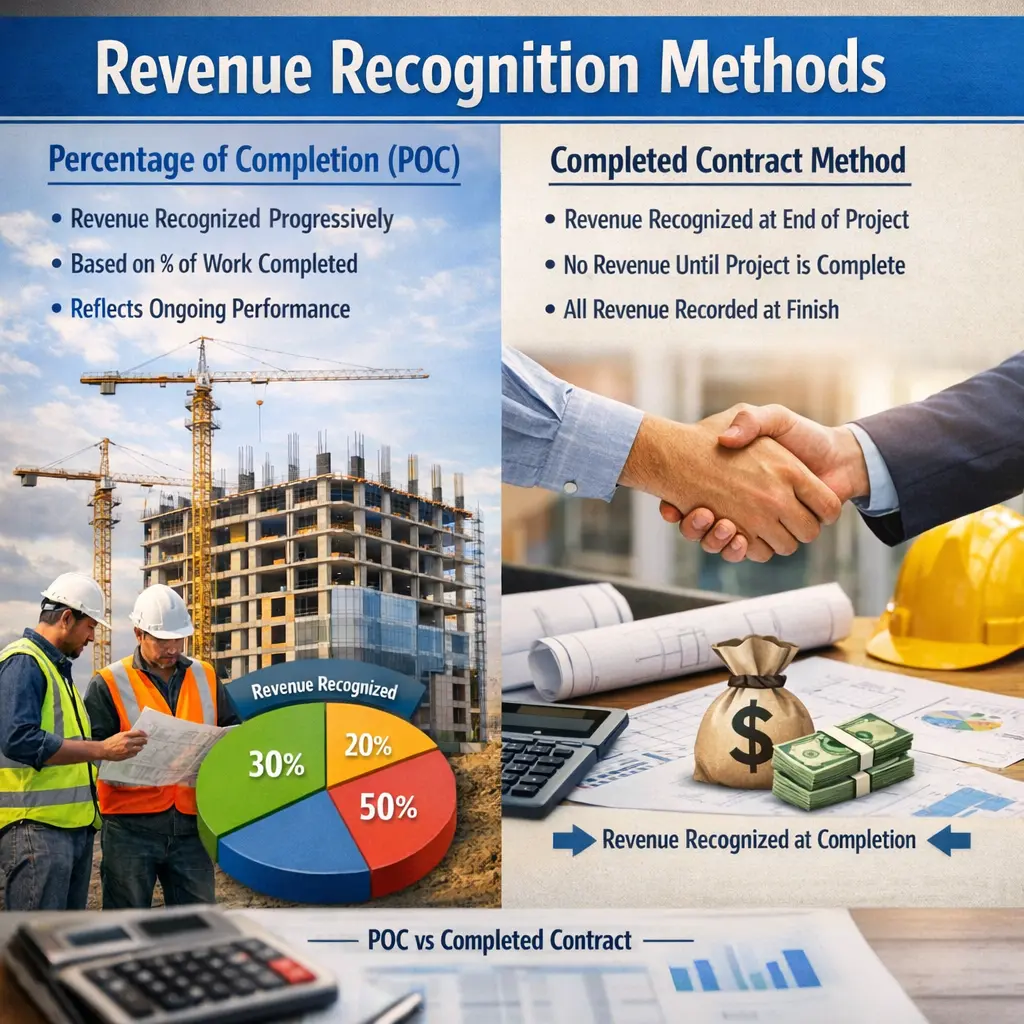

Revenue recognition methods determine when income from long-term projects is recorded. The Percentage of Completion (POC) method recognizes revenue proportionally as work progresses, matching income with incurred costs. In contrast, the Completed Contract method defers all revenue and expense recognition until the project’s completion. POC offers timely financial insights but requires reliable progress measurement, while the Completed Contract method is simpler but may distort interim financial results. Both methods impact cash flow reporting and business decision-making.

Revenue Recognition Methods (POC vs Completed Contract)

Revenue recognition methods determine when income from long-term projects is recorded. The Percentage of Completion (POC) method recognizes revenue proportionally as work progresses, matching income with incurred costs. In contrast, the Completed Contract method defers all revenue and expense recognition until the project’s completion. POC offers timely financial insights but requires reliable progress measurement, while the Completed Contract method is simpler but may distort interim financial results. Both methods impact cash flow reporting and business decision-making.

💡 Key Takeaways

- Understand how Percentage of Completion (POC) recognizes revenue as work progresses on long-term projects.

- Learn how the Completed Contract method defers revenue and profit until project completion.

- Compare the timing of costs, billings, and profits under POC versus Completed Contract.

- Identify factors that influence which method to use and the impact on financial statements.

❓ Frequently Asked Questions

What is Percentage-of-Completion (POC) method?

POC recognizes revenue and gross profit as work progresses, typically based on the ratio of costs incurred to date to total estimated costs.

What is the Completed Contract Method (CCM)?

CCM defers all revenue and profit until the contract is completed, with costs accumulated and recognized as a final sum at completion.

How do POC and CCM affect the timing of profit recognition?

POC recognizes revenue and profit earlier and steadily as work advances; CCM defers profit until the contract is finished, reducing interim volatility.

When should a company use POC versus CCM?

POC is used when the project’s outcome can be reliably estimated and collectibility is probable; CCM is used when outcomes are uncertain or reliable estimation is not possible.